Trying to decide whether to purchase term life or whole life insurance? Although term life insurance is the most common selection, which one is right for you? After you understand the difference, it will be easier to select a policy.

What Is Term Life Insurance?

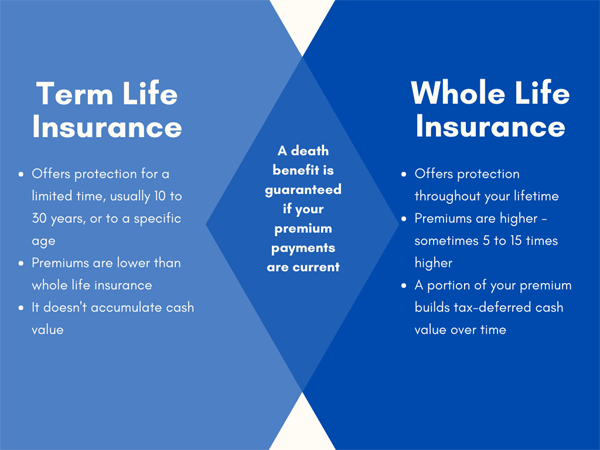

Term life insurance provides coverage for a specific period or term. Coverage periods are usually offered in increments of five years—usually between ten and 30 years. When the term ends, you can renew the policy, convert to a permanent policy, or let the policy expire.

- Premiums – Your age, health history, lifestyle, the term length, and the amount of coverage you want will affect your premiums. Term life insurance monthly premiums are less expensive than permanent life insurance premiums.

- Payout – Your beneficiary is guaranteed a payout if you die during the term of your policy.

- Cash value – Unlike permanent life insurance, term life doesn’t build cash value.

What term length should you choose?

Consider a policy that provides coverage until your dependent children, if any, have completed college and live on their own. At the end of the term, if you have fewer dependents, you can lower your coverage amount and save money on premiums. Or you can select a term that lasts until you retire if you’re leaving your retirement income to a beneficiary and can reduce your life insurance coverage.

What Is Whole Life Insurance?

Whole life insurance is a type of permanent life insurance. It provides coverage for your entire—or whole—life. Your beneficiary will receive a payout when you die. And the policy includes a use-it-or-lose-it cash savings account that accumulates over the years as you pay premiums.

- Premiums – Your age, health history, lifestyle, and insurance coverage amount will affect your premiums. Whole life insurance monthly premiums are higher than term life premiums—five to fifteen times higher.

- Payout – If your premium payments are current, your beneficiary is guaranteed to receive a payout.

- Cash value – Whole life insurance builds cash value over time. It’s a tax-deferred “living benefit” for you. If you die, your beneficiary will receive the death benefit, but the cash value will return to the insurance company.

It takes time to weigh the facts and decide which policy is best for you. Our post, Whole Life Insurance Policy – 5 Questions to Ask First, gives details on what you should consider before selecting whole life insurance.

How Much Life Insurance Do You Need?

Think about how much life insurance is needed to replace your income and care for your beneficiary and dependents if you die.

- Some experts recommend that you purchase life insurance that equals ten to 12 times your annual income.

- Other experts advise that you multiply your annual income times the number of years left until you retire.

- If you have a stay-at-home spouse, consider the cost of caring for your children or home if your loved one predeceases you. Get life insurance for your spouse, too.

Term Life vs. Whole Life – Five Questions to Ask Yourself

Take another look at the differences between term life and whole life insurance. Ask yourself the questions below. Confirm your reasoning with a licensed insurance agent who can help you compare your options, costs, and the long-term effects of the type of insurance you choose.

- How many family members will depend on my income for my entire life?

- Do I have debt that limits what I can afford to pay for premiums each month?

- What is the value of my assets and estate? Am I subject to an estate tax that I can pay with the tax-deferred cash value of a whole life insurance policy?

- Will I have enough savings to self-insure at the end of my term life policy, or will I need to renew or convert it?

- Do I have valid reasons to pay higher premiums for whole life insurance that builds cash value? Or can I invest elsewhere and get a higher return?

Start the conversation with Hunt Insurance of Raleigh-Durham, NC. Contact us today.