If you understand how life insurance works, it will help you decide if you need insurance, how much you need, and the type of plan you want. Without understanding the facts, you can over- or underinsure yourself—or do nothing at all. So how does life insurance work?

How Does Life Insurance Work?

Life insurance works by entering a contract with an insurance company. You will make regular payments (premiums) to the company for a life insurance policy that will pay a tax-free death benefit, or payout, to your beneficiaries if you die.

Do You Need Life Insurance?

You might need life insurance to leave enough money to help your spouse, partner, children, or other dependents pay for expenses if you are no longer living.

Some potential expenses include:

- Debt

- Education

- Everyday living expenses

- Funeral and burial expenses

- Income replacement

- Mortgage

- Out-of-pocket medical care

What are the Types of Life Insurance?

The main types of life insurance are term life insurance and permanent life insurance.

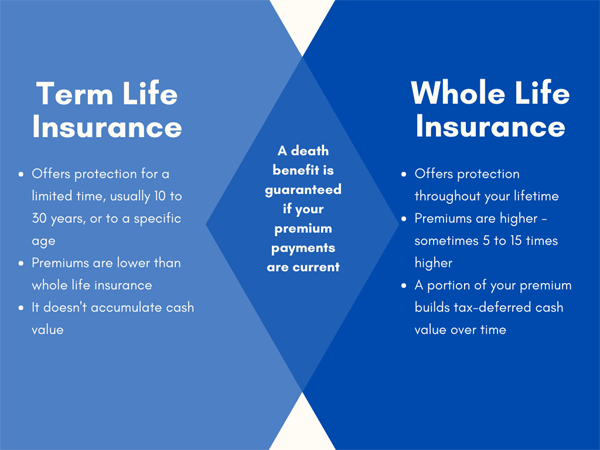

What is term life insurance?

Term life insurance is effective for a specific term, usually in increments of five years. When the period ends, so does the policy. But you may be able to renew it or convert it to a permanent life insurance policy.

Types of term life insurance

- Level term – Premiums stay the same throughout the term

- Increasing term – Premiums increase as you age

What is permanent life insurance?

Permanent life insurance does not have an expiration date. But lifelong coverage costs more than term life insurance.

Types of permanent life insurance

- Whole life – It is valid for your whole, or entire, life and has a cash savings component. Your premium payments insure you for a specific death benefit. Unused cash savings are not included in the death benefit.

- Universal life – The policy allows you to increase your death benefit, adjust your premiums, and combine cash value with your death benefit to increase the payout.

- Variable life – You can authorize your insurance company to invest your cash value in an account that the company manages. And you can use the investment earnings toward your premiums or the death benefit.

- Variable-universal life – You can adjust your premiums within the limits the insurance company specifies. And you can choose how to invest cash accumulation—which may result in gains or losses.

For a comparison of term and permanent life insurance, read our post: Term Life vs. Whole Life Insurance – How to Decide.

How Much Life Insurance Do You Need?

How much insurance you need depends on your survivors’ immediate expenses, long-term expenses, and the financial resources you already have. But many experts recommend that you multiply your annual gross income (before taxes) by 10 to 15. Ten to fifteen times your yearly income will give you an idea of the death benefit you need to care for your dependents.

Read our post, How Much Life Insurance Do I Need?, for details on the expenses to include in your calculation.

Can You Get Life Insurance If You Are Not Healthy?

Up to 50 percent of non-elderly Americans have a chronic illness. If you are one of them, you may wonder how your health will affect your chances of getting life insurance. But chronic illness does not automatically disqualify you from getting the coverage you need. Even a history of serious illness might not disqualify you. But it can increase the cost of your life insurance premiums.

For details on how your health affects your ability to get life insurance, read our post Can I Get Life Insurance Regardless of My Health?

Which Insurance Company Should You Choose?

With so many choices, how do you know which life insurance to choose? Look for a financially stable company with a long history of providing policies and paying death benefit claims. Although scores of high-quality life insurance companies exist, exercising caution always helps.

For easy-to-understand tips on selecting a company and policy that is right for you, read our post, Which Life Insurance Is Best?

Do You Need Help or Have Questions?

You are not alone. According to a Motley Fool article, one reason people say they do not have life insurance is not knowing what kind of policy to get. Hunt Insurance of Raleigh, NC, can help you navigate the decision-making process. Call or text us or complete our contact form to schedule a consultation or get a free, customized quote.