Forty-six percent of people living in the U.S. do not have life insurance. And one of the top reasons they do not have it is not knowing which insurance to get. If you are comparing life insurance companies and policies, how do you know which life insurance is best for your needs?

Which Life Insurance Company Is Best?

The best life insurance companies offer resources to help you understand your policy and when you need to adjust it. A stable life insurance company has a long, reliable history of providing policies and paying out death benefits.

Although many life insurance companies use names that convey strength, the Insurance Information Institute recommends verifying the company’s full name, location, and affiliation with other companies.

Also, research to find these facts about a company:

- Identity

- Reputation

- Ethics

- Financial status

- Product range

What is the quality of customer service?

Choose an insurance company that makes it easy to learn about the types of life insurance policies available and get help understanding them.

Look for these services:

- A comprehensive selection of policies

- Online articles and educational resources

- Online insurance calculators

- Accessible, knowledgeable, personalized customer service

What Is the Best Life Insurance Policy for You?

The best life insurance satisfies your reasons for purchasing a policy. Find a policy that fits your budget and offers enough coverage to care for your surviving dependents. The National Association of Insurance Commissioners advises that you select a policy that provides enough coverage based on your age and financial responsibilities.

Look for a plan that offers enough coverage to satisfy your potential needs:

- Replace up to ten times your income

- Pay off debt

- Care for aging parents or disabled dependents

- Pay for children’s education

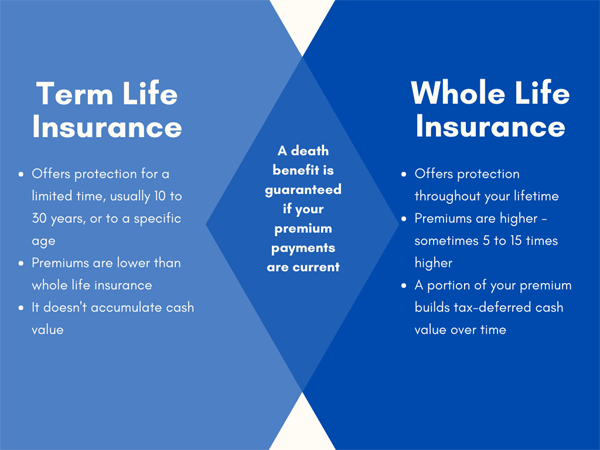

Term or permanent life insurance?

Term life insurance is in effect for a limited period, or term. Terms are set in increments of five (5, 10, 15 years, etc.) and can last up to 30 years. A whole life insurance policy lasts your entire life and builds cash value over time.

Before you purchase an insurance policy, ensure it fits your needs based on these factors:

- Your age

- The policy type and features

- The amount of insurance you are purchasing

- Cost of premiums

Many insurance policies offer riders—add-ons to enhance your policy. But riders will increase your premiums. Please read the post, Term Life vs. Whole Life Insurance – How to Decide for a comparison of term and whole life insurance.

In Raleigh, John Hunt of Hunt Insurance offers personalized assistance to help you identify an insurance policy that fits your needs and budget. Contact Hunt Insurance by phone or e-mail to request a consultation and a customized quote.

That’s the preference for most people. Explore your options, apply for life insurance, and receive it without an exam. If that’s how you feel, there are a few things to consider.

That’s the preference for most people. Explore your options, apply for life insurance, and receive it without an exam. If that’s how you feel, there are a few things to consider.